![]() “It takes all the running you can do to keep in the same place. If you want to get somewhere else, you must run at least twice as fast,” the Red Queen told Alice in Lewis Carrolls novel ‘Through the Looking-Glass’.

“It takes all the running you can do to keep in the same place. If you want to get somewhere else, you must run at least twice as fast,” the Red Queen told Alice in Lewis Carrolls novel ‘Through the Looking-Glass’.

Which brings me on nicely to the nonsensical ramptastic horse-shit that is currently being shouted, screamed, tweeted, whispered and posted by that well-known Aussie’ bullshitter extraordinaire, ‘Captain Ramptastic’ Mr David Lenigas and his twitter morons about Angus Energy (LON: ANGUS) which now has an £85M market capital valuation based on bread and butter assets currently being portrayed as the best thing since sliced bread.

Angus Energy

Angus Energy are a tiny micro-cap UK onshore oil & gas play they have two licenses in the Weald basin. Brockham and Lidsey. I’ve met their Chairman and Founder, Jonathan Tidswell. Had a few chats with him over the years. He’s a good guy. I like him. An able oil & gas man. The real deal. But even JT will be gobsmacked at the grossly ridiculous valuation of the company. Not to mention the massively over inflated promotion that has seen the SP rise to nearly 40p! Sadly, it looks to me like JT has fallen under the ‘Svengali’ influence of the purveyor of Australian bullshit ‘Captain Ramptastic’. And, why wouldnt he? JT’s stake is currently 16%, valued at a cool £13,500,000 a lot of Wonga…….

There are so many red flags it’s hard to list them all as I’d be here for two days writing them up. It’s that bad. I’ll stick to the main ones. Just to give investors the true flavour and a dose of reality, maybe even a dose of Epsom salts wouldn’t be remiss.

Red Flags

There are NO billions of barrels of oil coming onstream here at Lidsey/Brockham. (Just as there are NO billions of barrels of oil coming onstream at Horse Hill). Regardless of the ramping and gross massive over promotion, indeed there are no hundreds of millions of barrels and again indeed there are no tens of millions of barrels of oil coming on stream here. Now readers may rightly ask, how I can make those statements. Well it’s easy when you know how to research and fundamentally read a balance sheet.

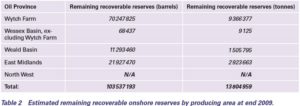

Starting with: The World Leading GeoScience Centre, The 2009 British Geological Survey results which ‘Objectively’ state; “The remaining recoverable oil reserves in the ‘whole’ of the Weald Basin were estimated at one and a half million tonnes. The conversion of that is 11,293,430 barrels, (Eleven million, Two Hundred & Ninety Three, thousand barrels of oil). Yes, folks that’s it 11.29M barrels of oil recoverable in the WHOLE of the Weald Basin! Investors and purveyors of ‘Subjective’ ramptastic shysterism alike should take note of what The British Geological Survey are saying. My money is on them.

Starting with: The World Leading GeoScience Centre, The 2009 British Geological Survey results which ‘Objectively’ state; “The remaining recoverable oil reserves in the ‘whole’ of the Weald Basin were estimated at one and a half million tonnes. The conversion of that is 11,293,430 barrels, (Eleven million, Two Hundred & Ninety Three, thousand barrels of oil). Yes, folks that’s it 11.29M barrels of oil recoverable in the WHOLE of the Weald Basin! Investors and purveyors of ‘Subjective’ ramptastic shysterism alike should take note of what The British Geological Survey are saying. My money is on them.

Now if you read through the NEX Bond £3,500,000 Memorandum, all 97 pages of it you’ll find so many red flags that one would be hard pressed to build sand-castles to stick them atop. I suggest each & every one of you read it otherwise each & every one of you will continue to be ‘Blinded’ by the shysterism being used to create the liquidity for the corporate hyenas to sell their stock and exercise their warrants. (More of which later in this epistle to the morons). The Truth will set you free and more than likely save you from the massive fall in SP that will hit once the ‘scores on the doors’ land vis-Ã -vis bopd. Not to mention the highly dilutive Placing that is currently being lined up. Read HERE.

Brockham & Lidsey Production

The truth of previous oil production is Lidsey 25bopd; (12 bopd net to Angus). Brockham 35 bopd (21 barrels net to Angus). After the drills/workovers production according to the Xodus CPR, could be; Lidsey 279 bopd (167bopd net to Angus) Brockham 93bopd (55bopd net to Angus) The best-case scenario and I’m being really generous here, not including the decline rates which are over 50%, is 223bopd net to Angus. The on-going OPEX & CAPEX needed to keep production at this level would in all probability render them close to un-economic. These are facts that have been deliberately obfuscated by ‘Captain Ramptastic’. Jonathan Tideswell himself has stated “Following the conversion of the Brockham well and drilling of the Lidsey-2 horizontal producer the Group expects to have a net production by the end of the next reporting financial year of approximately 150bopd, in line with the P50 production guidance as given by Xodus in their CPR”. Now that’s an awful big change from the over promoted IPO presentations and the ramptastic shite of Mr David Lenigas, is it not? Not exactly earth shattering, is it?

Angus Fundamentals

Angus Energy is grotesquely overvalued. A market cap’ of £85,000,000 for a company that may produce 150 barrels of oil from piss poor Bread & Butter UK onshore assets is Alice through the Looking Glass, madness.

The fundamentals here are thus; Angus had on Initial Public Offering (IPO) £3,050,000 (net) in cash. They then raised a further £2,000,000 (gross). As at 31 March 2017 the Company had cash of £2.3M. Again, being generous, ’cause I’m a generous type, I won’t take out the fees of at least £100K from the gross £2,000,000 raised in February 2017. The six-month cash-burn up to March 31 2017 is £2,750,000, which equates to a staggering £458,000 per month spent up to March 2017. Cash was £2,300,000 as of March 2017, 6 months have now passed. So how much of the £2,300,000 is left? Answer Zippo!

Even if you put their cash burn down to £350,000 per month for the period up to Sept’ 2017 this would leave the company with net cash of circa £200K. Are you all getting the picture now? Do you smell the placing?

I won’t put in any liabilities etc. Let’s make it really simple. Asset Value booked in at £2,300,000, cash in hand circa £200,000. Total £2,500,000. Production zippo. The ramped up ‘Hope Value’ is a jaw-dropping £82,500,000. Let’s put some common-sense on the ‘Hope Value’ and assign it a ‘generous’ £5,000,000. That would give a Market Cap’ of £7,500,000 extrapolated into a share value of 3.10p. Let’s double the ‘Hope Value’ to £10,000,000 for fun, 6.2p gives a £12,500,000 Market Cap’. The disparity between the current reality of the Net Asset Value for a micro-cap that may produce 150-223bopd that will decline substantially is humongous! Angus Energy isn’t worth 35p/36p a share! It’s a ramped up uber non-producing micro. With a potential 150-223 bopd. That’s it folks! The value of their shares is 3p at best!

“Hang on you shorter Levi, What about the £3.5M NEX Bonds?”

Firstly, I do not short. That is a fact. I report it as I see it. Anyone with half a brain who takes the time to read the NEX Bond Memorandum will learn that the Bonds can only be issued in tranches and those tranches cannot be issued until, I repeat ‘until’ production starts! Which is why there’s been 7 RNSs, each one announcing to the ‘lumpenproletariat’ (Google it) that the date of issue has been put back. Those Bonds are secured against ALL the companys’ assets, production and SHARES. No production No Bond issue. Can you smell the Horse-shit now?

There will be no Bond issue until production starts. Tranches will be issued in respect of how much free cash is generated which is minimal on 150-223bopd. The AIM Cesspit professionals know there’s a Placing about to drop. It’s the great unwashed, who are being spoon fed Kimmeridge Black gold fairy tales, that don’t!

Now I’m hearing whispers & rumours that investors are being soothed with sweettalk from people who may be from the company or not, or involved in some way with the company, or not, intimating through ‘back-channels’ that they won’t Place. This is ‘porkypies’. I hope that those who may be getting told there’s no Placing, fully funded etc. Upon getting shafted immediately report ‘those’ who may have told them such utter lies. You wont have long to wait. A Placing is imminent.

Kimmeridge Fairy Tales

The share-price is 35.75p it has been ramped up to high heaven. This is a deliberate ploy by the Lenigas ‘Kimmeridge Fairy Tale Gang’ operating out of the corporate Boiler Room that is Jermyn Street London. The mutterings, allusions & twittering’s of untold Kimmeridge clay/shales black gold, billions upon billions just around the corner Tweets, BB posts, CPR and RNS teasers of Kimmeridge tests, allusions to UKOG etc. Nudge! Nudge! Wink! Winks… This has been done by the promoters to deflect away from the cold hard financial reality that is Brockham & Lidsey. These are ‘bread & butter’ onshore assets and they will never ever produce anything other than piss poor, OPEX & CAPEX expensive, oil that declines very rapidly and needs cash thrown at them to maintain production.

‘Captain Ramptastic’ David Lenigas ‘Modus Operandi’

Ramptastic Bullshitter X 140+ Companies

Now I don’t propose to go in-depth into the Modus Operandi in this piece, that will be dealt with in greater detail over the coming months. Brief over view is all that’s needed here. ‘Captain Ramptastic’ has been involved with over 140+ companies in various roles, that figure is probably much higher.

Each and every one of those companies has been massively over-promoted whether that be the greatest gold mine in Wales: Stellar Resources. The world changing eco Boiler: Inspirit Energy. A super dooper airline: Fastjet. Feeding the African continent: Afriag. Cuban Oil & gas oops tourism, oops again, now medicinal cannabis: Leni Gas Cuba. Untold Mexican lithium riches of the battery world, and the Internet of Things: Rare Earth Minerals. Trinidadian black gold riches: Leni Gas & Oil. Tanzanian, Spanish & global portfolio of oil & gas and now helium (Laughing Gas): Solo Oil. The greatest African conglomerate of hotels, ports and agricultural businesses: Lonrho. Onshore UK billions I tell ya billions of barrels of oil in the Weald: UKOG. Diamonds are forever: River Diamonds. That metamorphosed into a Bonanza gold mine: Vatukoula Gold Mines. Fly me to the moon crash and burn: Norse Air Limited. More rare earths. So rare I’ve got two companies: Bacanora Mineral Ltd. Rub in my magic face cream it works wonders for anti-aging: Evocutis. That didn’t work let’s change it to investing in resources: Gunsynd. Now I could go on and on with this list but as I said that’s for another major expose on David Lenigas. But I think that gives you a taster of what this fooker is all about. Ramp, Pump, Dump, Place, Rinse, Repeat.

Each and every company that this man is involved with is ramped to death and each and every company ultimately bombs. Peppercorn stock and warrants are sold into the liquidity that the ‘Over Promote’ causes. How many Angus CONsultants warrants does he have? How many shares has he sold into the pump? David has said he doesn’t have any. Is this the truth? Bearing in mind Doriemus and his recent UKOG warrants forced admission. Placings are used to refill company coffers to pay ‘Captain Ramptastic’ and his cohorts’ Executive Remuneration and to keep the story going of untold riches for investors. Dilutions, placings and consolidations. The people involved with the ownership of the companies, such as the 4% of the UK Energy needs for the next 30yrs ‘Captain Ramptastics’ BB/HH UKOG fantasy, are a complex web of companies/shareholders, a trademark of Lenigas’s affairs. The dreams of UK Investors are always left shattered to smithereens. The transference of wealth from the naive investor to the Corporates complete. Job done Mr. Lenigas quietly exits and leaves the company mouthing some bullshit. Not one of the companies has ever made it to the Big Time. Angus Energy are but one of the many ramps.

David Lenigas has made tens if not hundreds of millions of pounds massively over promoting piss-poor AIM penny stocks. He’s good at what he does. A truly gifted Promoter but that is all he is a Shyster Promoter. The life style is large, Yacht in Monaco, Offices in St James City of Westminster, property in Monaco, properties in London, Australia, 1st Class flights, hotels, bulging bank accounts etc. Tis a champagne lifestyle. He uses the same people over and over again. The cross pollination of companies and directors is well known in the City of London. The usual suspects take their cut and get ready for the next one.

Now if the Fat Promoter would like to challenge that in the High Courts of London then go for it David. I will gladly oblige you and expose you for exactly what you are: A corporate Aussie’ bullshitter, a scammer taking advantage of gullible naive UK Investors, citizens of my country. Bring it on Mr Lenigas.

Angus Energy. Without a ‘G’ is Anus.

Compare An(g)us Energy to let’s say mmmm…… Zenith Energy (LON: ZEN). They’re a producer churning out 350bopd, their Azerbaijan field is way bigger than both of Angus’s and they have half the shares in issue than Angus. The current share price is 7.25p. The Market Cap’ is circa £9M. The difference is that Angus have no production, yet, Zenith have. Zenith doesn’t have the sustained massive ramp/promote. Angus does. By the way Angus only just scrapped onto AIM as a marginal company based upon their IPO and what Xodus says in the NEX Bond Memorandum.

That’s not all Xodus say, in their Executive Summary, page 29, “Xodus has read the Nutech report. Although it presents an interesting comparison with the Horse Hill-1 potential, Xodus’s view is that there is insufficient information available to provide a credible assessment of the petroleum volumes in place and/or recoverable from the deeper reservoirs that is in accordance with the PRMS standards and AIM guidelines” they have put clear water between the wild speculation and manipulation that is being orchestrated on the ‘Billions I Tell Ya’ of Barrels Kimmeridge ‘Hail Mary’ play. Furthermore, they conclude Page 31, that the economics are thus: “An economic analysis was carried out on the Reserves on the Brockham and Lidsey fields. The results are provided in Table 1.4. The Reserves have a small positive Net Present Value (NPV). Now that’s not exactly a ringing endorsement is it folks?

Apart from the fundamentals, which are desperate, Angus have also got to pay their share of Holmwood Licence. Part of the agreement to acquire 12.5% of the Holmwood Licence, the Group agreed to pay certain historic costs incurred by Europa since 1 February 2016 (representing £26,563 of net cost to the Group) and 25% of the costs of the Holmwood-1 exploration well up to a gross well cost of £3,200,000 (representing a potential net cost of £800,000 to the Group) along with certain further costs the details of which are set out in the Xodus Memorandum. Placing? No of course they won’t they’ve got a ‘Money Tree’ from Teresa May! You’re having a laugh aren’t you? “It is therefore difficult for prospective investors accurately to evaluate the Company’s business and future prospects. There can be no assurance that losses will not occur in the short term or that the Company will be profitable in the future“

It gets worse does Xodus Page 45 Contractual documentation: “The Angus Group does not have in its possession executed counterparts of certain of the contractual documents relating to the acquisition and disposal of interests in, and the operations of, its oil and gas assets (including the Licences), the terms of which are referred to in paragraphs 2, 3 and 4 of Part I and 13.3 and 13.7 of Part VI of this document”. On page 51, this is a real killer and an eye opener “Exploration, development and production activities are capital intensive and inherently uncertain in their outcome. As a result, the Company may not generate a return on its investments or recover its costs and it may not be able to generate cash flows or secure adequate financing for its discretionary capital expenditure plans”

I could talk till the cows come home extrapolating literally dozens if not hundreds of caveats that ‘Captain Ramptastic’ doesn’t want you to read. What we have is a massive, orchestrated pump and dump of a bread and butter asset/s using smoke and mirrors while intimating Kimmeridge black gold, cherry picking a hypothesis. The Xodus report makes it crystal clear. There will be no Kimmeridge shale black gold. What the Angus Rampers are doing is constantly ‘alluding’ to Horse Hill & Broadford Bridge which is in itself a crock of shit.

If I was in profit here now knowing what I do I’d get the hell out and sell. That’s what ‘Captain Ramptastic’ and the Horse Hillsters are all doing. Theres a Placing coming and make no mistake about it. It is Imminent!

Massively over hyped, worth about 3p on a drug fuelled drunken day!

Remember what the Police always tell people to avoid being a victim of scams. “If it sounds too good to be true it probably is” On that cautionary saying I shall leave you all to ponder this; The David Lenigas track record V The British Geological Survey. Place your bets..

Viva

Viva

Daniel.

Spoke to my broker this morning. She says that ‘”all probability ANGS financials are threadbare” that they need funds. Good piece Dan. Have followed you on twitter.

David Lenigas is a crook. Its as simple as 1 2 3. I recall the massive pay rise he tried to sneek through at Lonrho. No matter what you write brokerman he’ll just carry on raping idiot mug punters. He’s horrible individual.

Graeme Dickson of optiva behind Angus run for the hills

Well blow me down. There was I thinking BMD was little more than a loud-mouthed, self-aggrandising, self-serving, incoherent, uneducated bully with a criminal record and then I read this.

Not only does the man write well but he puts to shame redbrick-educated Tom Winnifrith who is incapable of publishing a sentence without rendering it incomprehensible with typos.

Worse, I agree with every word. I am therefore revising my opinion of BMD…to coherent.

Actually, what I am really posting about is the imminent demise of the fraud, Lenigas. The Canadian and UK regulators are all over the fraudulently misleading investor presentation and related publicity used by LGC Capital last month to extract $3m from Canadian mugs. And one of his directors who worked on it has just resigned.

The presentation, on the LGC website, has been hastily edited and republished twice in the past 24 hours after I alerted the CEO that it amounted to securities fraud. But I kept the original August version and have circulated it to all the regulators, including the Mounties (who always get their man).

Check your Twitter feed for details and links.

Lenigas is a bare faced liar. ShareProphets exposed him many times for lying through his teeth. Seasoned investors know all about the Aussie crook. We stay well away. Only the muppets and mugs swallow his horse Hill shit!

Superb piece Dan. Excellent. I sold Angus at 34p soon as I read. It’ll go down to sub 10p.

So. What about A Egdon resources then?

What about them?

I wish I had listened to you..pre November 17th.Lies,lies and more lies..

Having read the article, i decided to check the source re Weald Basin … http://www.bgs.ac.uk/research/energy/shaleGas/wealdShaleOil.html

The estimate is in the form of a range to reflect geological uncertainty. The range of shale oil in place is estimated to be between 2.20 and 8.57 billion barrels (bbl) or 293 and 1143 million tonnes, but the central estimate for the resource is 4.4 billion bbl or 591 million tonnes.

What don’t you understand about kimmeridge clay oil? It’s unrecoverable. Shale has to be fracked. Which is why every Major Oiler has walked away. Kimmeridge clay doesn’t allow oil to flow. Best case on a frac is 1/2% recoverable. Your figures are for the whole of the weald.

There’ll Be no fraccing in the Weald. EVER!!!!

The fraudulently misleading presentations and assurances by Vonk and rhe Angus BOD have wiped out quite a few private investors. From promising 279 bopd at Lidsey and then only producing 40-to reassuring investors a week before the placement that “Lidsey would be entirely self-funding”.

Now to top it all,a new placement to fund drilling in an oil field already abandoned by Cuadrilla and Canocco phillip as uneconomic.Totally contradicts it’s declared strategy of “minimising risk”.

A few of us Angus investors have decided they can’t get away with this any longer.

I have spoken to a leading firm of city barristers who have told me we have a viable and convincing case for action against Angus for negligent misrepresentation.

If you woukd like to consider joining a group action & woukd like info contact me

Keither197@Gmail.com